February 2023 – Manager’s Thoughts

Author: Joe Maas, Chief Investment Officer, SPG Advisors LLC

Financial Markets

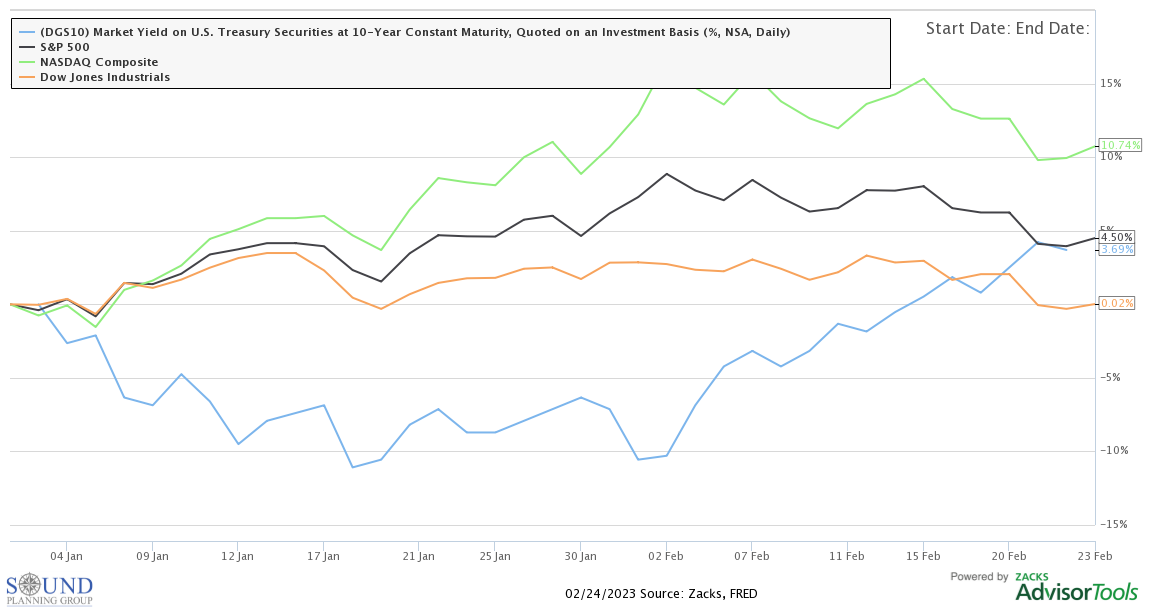

Investors ended the last full week of February concerned over a likely more sustained period of quantitative tightening, as Fed members speak out and more economic data comes in. Year to date, as of Thursday, February 23rd, the S&P 500 is up +4.5%, the Nasdaq Composite is up +10.7%, the Dow Jones is flat, and the 10 year US treasury yield is up +3.7%.

Market News

Existing Home Sales. This week began slow with economic data, with the January existing home sales coming out on Tuesday. Existing home sales in January fell -0.7% from December, coming in 90,000 short of expectations at 4.0 million homes sold. From twelve months ago, sales are down a whopping -36.9% across the US.

The median sales prices of existing homes increased a mere +1.3% year over year from January 2022 to $359,000. This comes as rates for a 30-year fixed mortgage near 7%, making monthly payments a fair bit higher than one year ago, when rates were under 4%. Inventory increased to a supply of 2.9 months’ worth of sales, nearly double of what inventory was one year ago.

One thing from the existing home sales report is clear, the housing market is cooling off, primarily from higher interest rates, but also from the US economy cooling off subsequently.

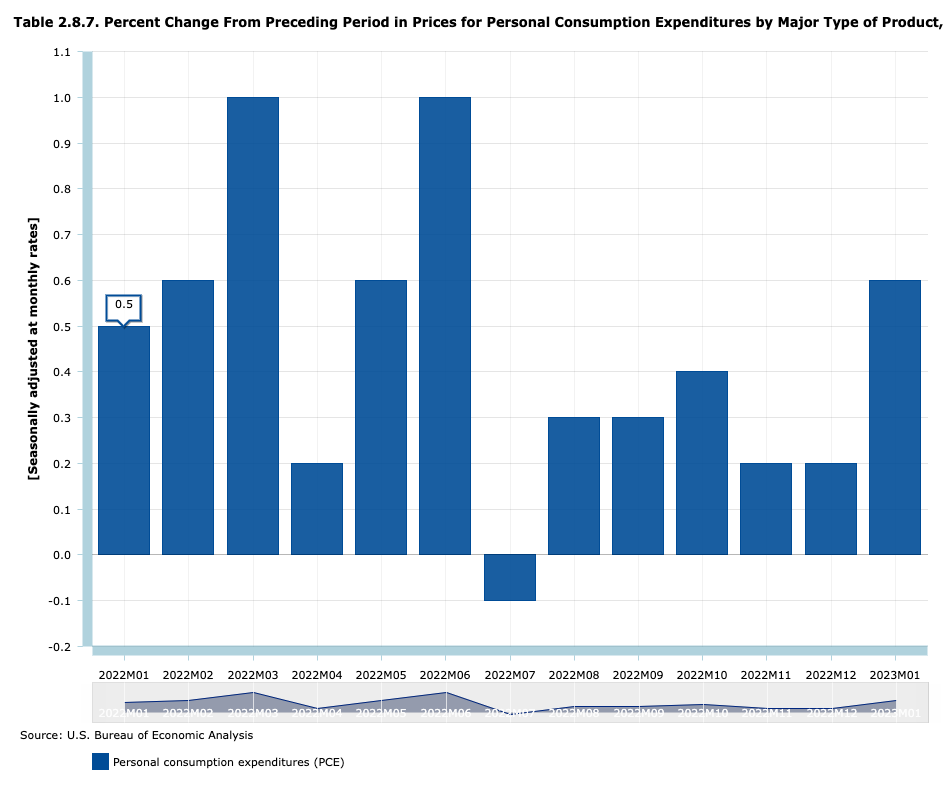

Personal consumption expenditures (PCE): Friday morning, the BLS rolled out a slew of vital economic data, including the Fed’s favorite inflation metric, PCE inflation. January PCE came in at an annual inflation rate of +5.4%, up 10 points from December’s +5.3% reading. This follows a hot CPI reading last week, yet still was a surprise to investors.

January’s Core PCE inflation came in similarly hot at +4.7% year over year, versus December’s weaker, 4.6% Core PCE inflation. On a month over month basis, both PCE and Core PCE inflation came in at a roaring +0.6% rate, up from December’s +0.2% PCE and +0.4% Core PCE inflation rates. These higher inflation rates spooked investors and sent equities down over 1% before market opening on Friday.

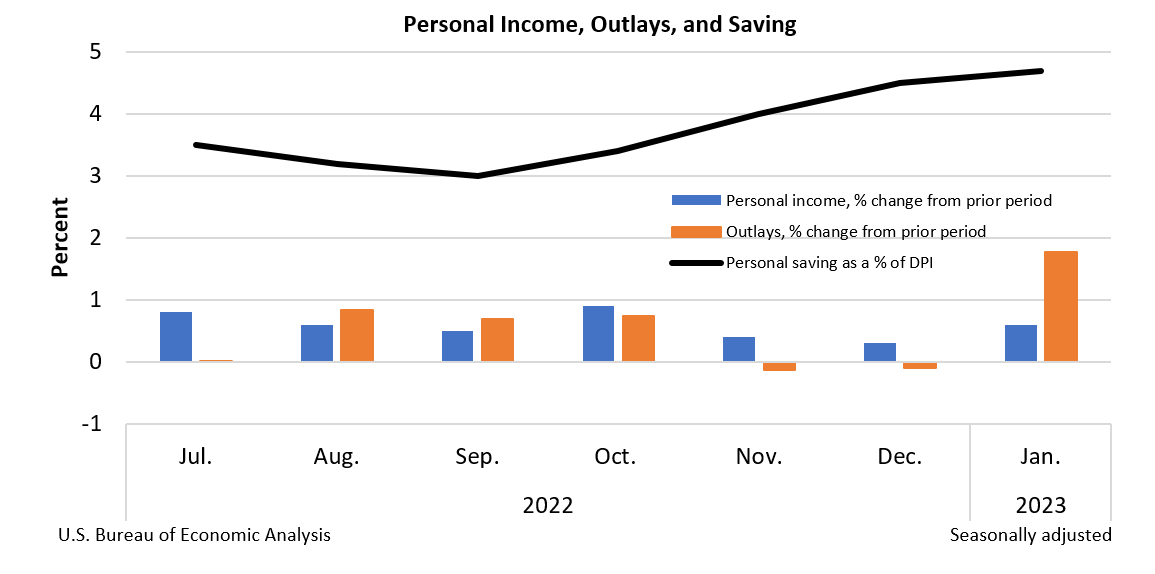

Personal Income, Spending, & Saving. In addition to the BLS’s PCE inflation report, personal income, outlays, and savings for the month of January came out Friday morning too. Outlays or spending increased a whopping +1.8% from December, much higher than expectations of 1.4%. Personal income increased a slower, +0.6% month over month in January, compared to estimates of +1.0%.

Consumers’ personal savings rate rose to 4.7%, up 20 bps from December’s 4.5% savings rate. From this report, we see that consumers are still feeling higher prices and thus higher spending necessary from one year ago. At the same time, wage growth is slowing a fair bit and consumers are saving more in reaction to all of this, on top of economic uncertainty.

Summary

Stronger inflation, a slowing housing market, slowing income growth, and higher savings rates don’t bode well for the economic uncertainty we are already facing. This uncertainty drove equity markets down this week, chipping into the year-to-date rally we saw in January and early February.

On Thursday, we rebalanced most portfolios and we maintained cash in the appropriate portfolios as well as initiated a small, short position in equities and fixed income in the Sailboat portfolios. We will continue to adjust all portfolios as the data ebbs and flows. In this type of market, our move from bull to bear is fluid and we expect this volatility to continue throughout 2023. As we have been communicating, our overall posture is to be cautiously hedged.

We look forward to continuing to monitor this constantly shifting macroeconomic environment for our clients.

-Joe Maas

The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Our advisors can meet with you to discuss your retirement plan.

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.