Market Update – September 29th, 2023

Author: Joe Maas, CIO, SPG Advisors, LLC

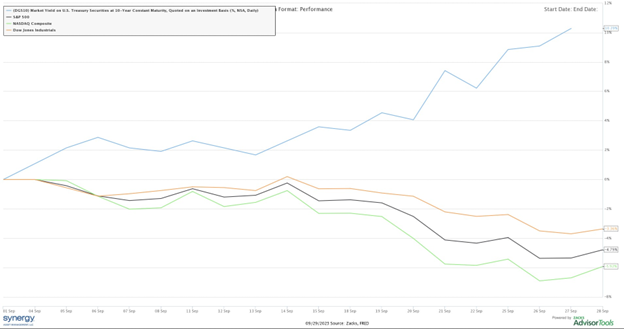

| Financial Markets: Historically, September tends to be a weaker month for stocks, and that trend was true this month as equities suffered. As of close Thursday, September 28th, the 10-year US Treasury yield gained 10.29%, while the Dow Jones Industrial Average fell -3.36%, the S&P 500 fell -4.79%, and the Nasdaq Composite fell -5.92% for the month. The most notable catalyst of this drop in equity markets was the Fed’s September Summary of Economic Projections, which showed that the Fed may want to keep higher rates for longer in 2024 and 2025. |

|

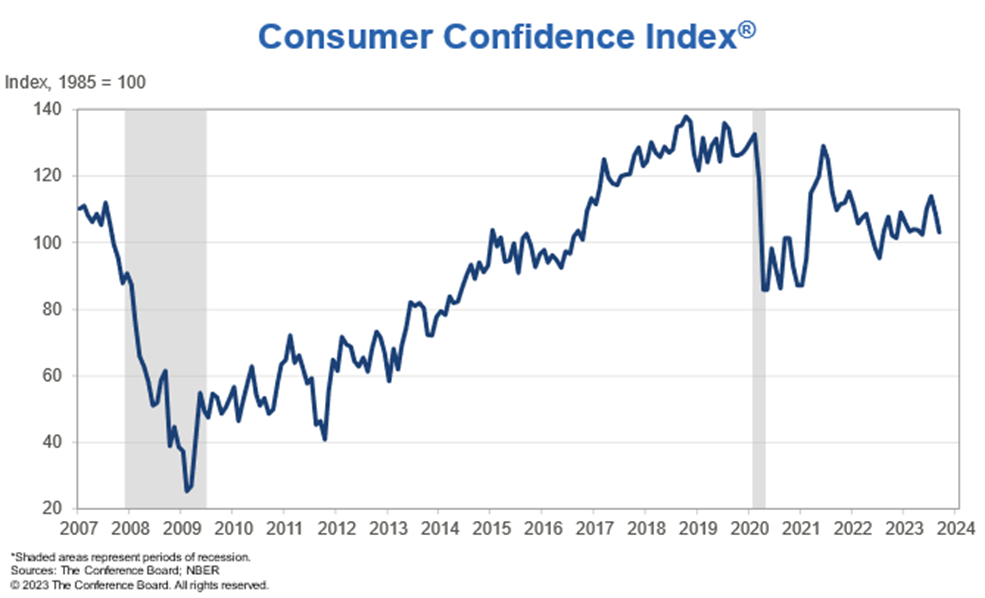

Market NewsSlipping Consumer Confidence. September’s Consumer Confidence Index slipped for the second month in a row to 103.0, down 5.2% from August’s index. Consumers’ responses to the index largely reported that higher gasoline prices, paired with the political uncertainty of a possible government shutdown on Sunday, October 1st, and the pressure of higher borrowing costs led to this lower confidence index. Also from the index survey, the share of respondents reporting that their current family financial conditions are “good” has fallen, while those who report their family finances were “bad” has risen. Other data points outside of the Consumer Confidence Index have similarly indicated this, with revolving credit (which is largely credit card borrowing) up +9.2% in July compared to a year ago. Consumers are beginning to materially feel the weight of this tightening cycle and data is confirming it. |

|

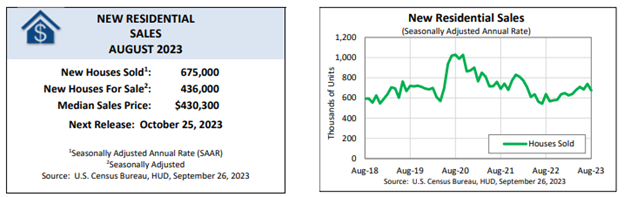

New Home Sales. August’s new home sales came in almost 4% lower than expected this week, at 675,000 homes sold. The median sales price was $430,300, leaving only 436,000 new homes remaining on the market as of the end of August. New builds have been a significant source of supply in this tight market, so fewer new homes being built and sold is not good news for those hoping for real estate prices to settle down. With continued limited supply, residential real estate prices will likely remain sticky, as those with lower mortgage rates who bought at lower prices stay in their home longer than they may have wanted to. |

|

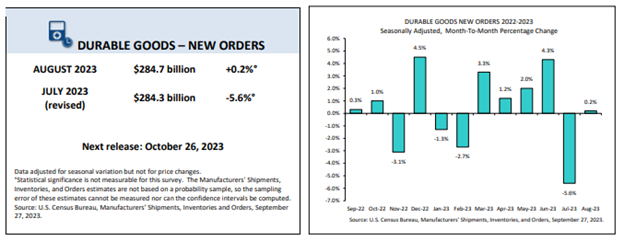

Durable Goods Orders Come in Strong. Despite the manufacturing sector showing weakness in certain regards, durable goods orders rose +0.2% MoM in August, after a notable monthly drop of -5.6% in July. Economists were expecting another monthly drop of orders in August, however this better-than-expected reading on durable good orders shed some positive light on the manufacturing sector. Much of the growth in new orders stemmed from defense purchases, along with machinery purchases, both driving up the total monthly increase in new orders. We look forward to continuing to monitor the manufacturing industry as we tilt in and out of certain sectors in our portfolios. |

|

PCE Inflation. Core PCE inflation fell below 4% for the first time since 2021, to an annual rate of 3.9% in August, while Headline PCE inflation rose to 3.5% YoY. On a monthly basis, costs of goods fell -0.2%, while costs of services rose +0.2%, ultimately causing both Core and Headline PCE to rise a slight +0.1% for the month. Similar to the CPI, higher energy costs also led PCE higher for the month, something that may continue through the end of the year as expected production cuts will likely continue to limit supply and drive prices higher for energy. |

|

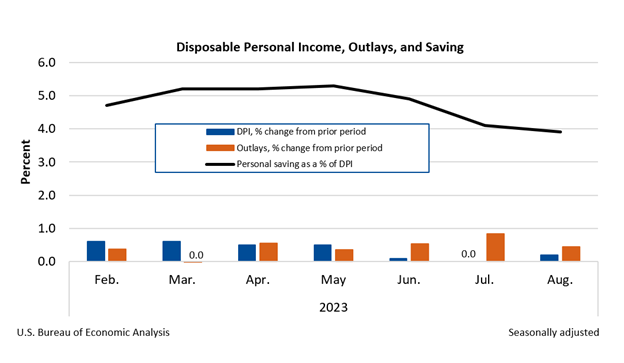

Personal Income, Spending, & Saving. Personal income increased +0.4% in the month of August, while personal spending rose +0.4% alongside it. Savings rates fell again in August, to just 3.9% of disposable personal income, which is not great for the consumer in the midst of uncertain economic conditions to come and higher revolving credit usage (credit cards). This month’s report demonstrates again that the consumer is starting to feel the lagging impacts of higher interest rates as they spend a higher proportion of their income, save less, and feel less secure (see this month’s Consumer Confidence above). |

|

Summary We closed out the month of September with a week for the bears, as we avoided a government shutdown and face the realities of a slowing economy. Consumers are feeling less confident in the economy, while new home sales came in slimmer than expected. Durable goods orders brought a positive surprise for the manufacturing industry and PCE inflation came as expected, showing an increase in the cost of services MoM and a decrease in the cost of goods. Add to this that consumers are saving slightly less and continuing to spend, we may begin to see the lagging impacts of higher interest rates soon. In any case, we will continue to monitor the economy and markets actively in this unique environment. We appreciate your continued trust. |

Thank you,  Joseph M. Maas, Joseph M. Maas,CFA, CFP®, ChFC, CLU®, MSFS, CCIM, CVA, ABAR, CM&AA The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Our advisors can meet with you to discuss your retirement plan. |

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.