Market Update – September 15th, 2023

Author: Joe Maas, CIO, SPG Advisors, LLC

Published September 15th, 2023

Financial Markets

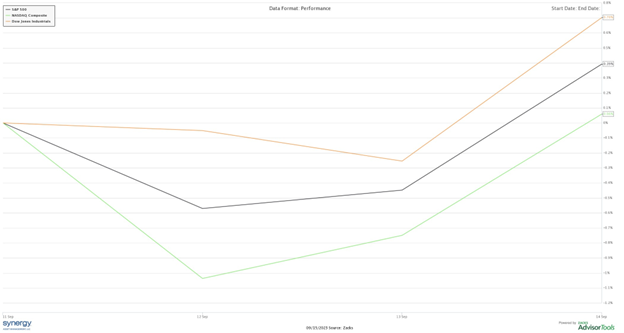

Markets found solace this week, as equities rose slightly amidst a backdrop of sticky inflation data, an exciting IPO, and a record-breaking inverted yield curve. As of close on Thursday, September 14th, the Dow Jones Industrial Average gained +0.7%, the S&P 500 gained +0.39%, and the Nasdaq ended flat with a thin gain of +0.06% for the week.

Market News

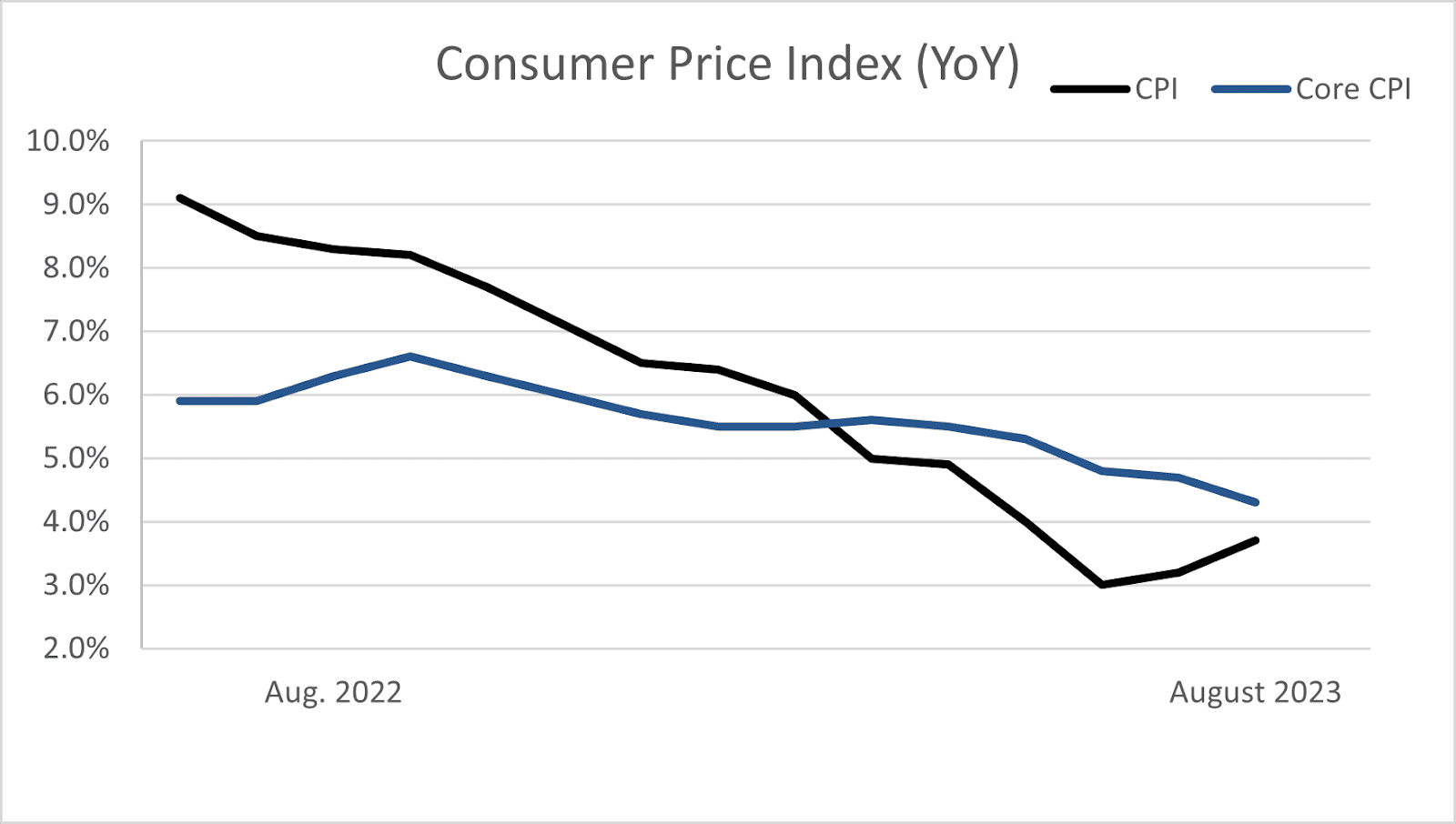

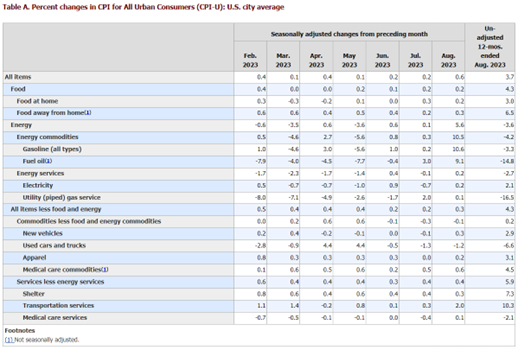

August’s Hot CPI Print. Headline CPI for August surprised economists to the upside, clocking in at an annual Headline rate of 3.7%, up 50 bps from July’s lighter 3.2% inflation rate. On the other hand, Core CPI, that excludes food and energy, settled to an annual rate of 4.3% in August, down slightly from July. Month over month, CPI was up +0.6%, while Core CPI rose a slimmer +0.3%, however monthly data came heavily skewed by just one category – energy.

Energy led inflation higher in August, marking a +10.5% monthly increase in energy commodity prices, which may persist as Saudi Arabia claims to be cutting production by 1 million barrels per day through the end of December. Other categories driving CPI higher on an annual basis included transportation services (+10.3% YoY), shelter (+7.3% YoY), and food away from home (+6.5% YoY).

On the contrary, used vehicles (-6.6% YoY), energy (-3.6% YoY), and medical care services (-2.1% YoY) brought inflation lower in August. This higher CPI print from August may largely be a result of geopolitical pressures driving energy prices up, however we will continue to monitor inflationary trends in order to best execute portfolio decisions based on our economic views.

Source: BLS

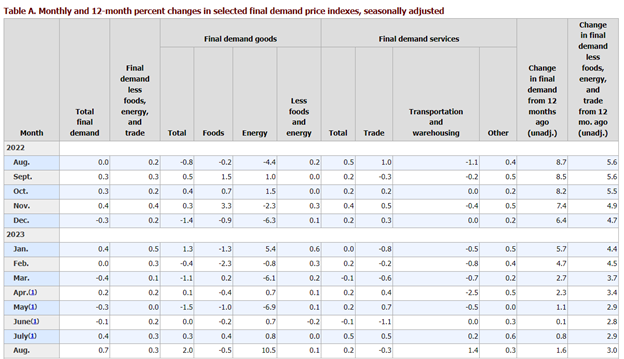

Producer Prices Rise in August. Monthly PPI rose +0.7% in August, almost twice analysts’ estimates of +0.4%, while monthly Core PPI rose a slimmer +0.1%. On an annual basis, August’s Producer Price Index rose +1.6%, the highest reading since April, while Core PPI rose +3.0%. Similar to CPI, producers faced increased energy costs, up +10.5% month over month, along with higher transportation and warehousing costs, which were up +1.4% in one month. Food costs to producers fell -0.5% MoM and trade costs fell -0.3% MoM, preventing the PPI from coming in even hotter.

Source: BLS

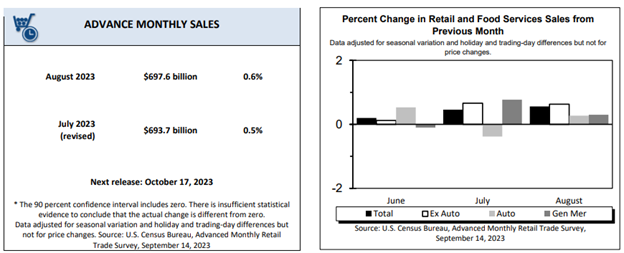

Retail Sales. August’s retail sales came in stronger than expected at a monthly increase of +0.6%, but were only up +1.6% from August of 2022, totaling $697.6 billion for the month. Food services and drinking establishments led sales higher, up +8.5% from a year ago, showing consumers’ continual preference for service and experience focused spending. As we near October, when student loan repayments reenact for many borrowers, it will be interesting to see how the consumer chooses to spend their wallets on goods and services.

ARM IPO. In one of the largest IPOs since the recent slowdown, ARM Holdings, a leading chip design company based in Great Britain, was listed on Thursday and got the attention of investors worldwide. Priced at $51 per share, ARM closed 22% higher in its first trading day, as the company also revealed it sold shares directly to its top customers including Apple, Google, Nvidia, Samsung, AMD, and many others. Coming out of an unusually slow IPO market, we look forward to seeing if capital markets start to regain traction in opportunities for new listings.

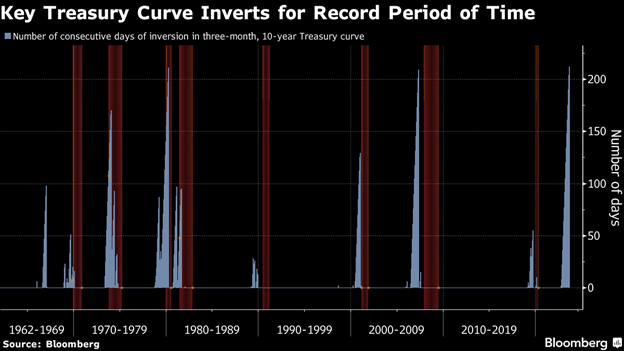

Inverted Yield Curve. The 10-year to 3-month US Treasury yield spread beat a record this week for the longest inversion of rates the US has ever seen, with the 3-month yield being higher than the 10-year for 212 consecutive trading days as of Thursday, September 14th. Historically, an inverted yield curve, one where short-term yields are higher than long term yields, has been a tell-tale sign of an economic slowdown to come. In fact, over the last 60+ years, every instance of a longstanding inverted yield curve was followed by a recession of some magnitude. Now this is no guarantee of economic conditions to come, however it is a great leading indicator economists will tend to glean over in the uncertain economic era we find ourselves in.

Summary

Despite a variety of bearish inflationary data including CPI and PPI, we saw equity markets close higher for the week as of Thursday. Inflationary data rose more quickly than expected as energy prices weighed heavily on both consumers and producers in August. Retail sales demonstrated that consumers are not afraid to spend by any means, as preference continues to shift towards service-focused goods. A hot new IPO listing, ARM Holdings entered the market this week as a win for the bulls, while the continually inverted yield is flashing warning signs about economic conditions to come.

We appreciate your continued trust.

Joe Maas

Joseph M. Maas,

CFA, CFP®, ChFC, CLU®, MSFS, CCIM, CVA, ABAR, CM&AA

The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Our advisors can meet with you to discuss your retirement plan.

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.