Market Update – October 6th, 2023

Author: Joe Maas, CIO, SPG Advisors LLC

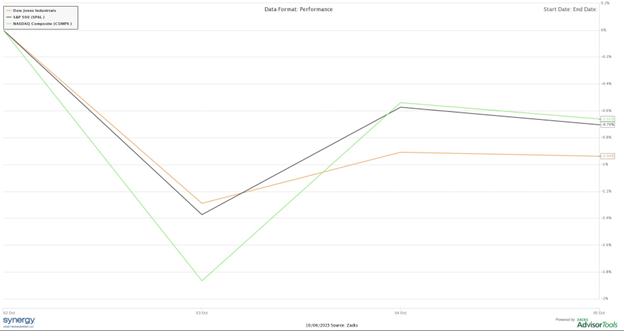

Financial Markets The first week of October came full of economic data and movements in interest rates, as equities saw large swings but ultimately ended lower. As of close Thursday October 5th, the Nasdaq Composite fell -0.66%, the S&P 500 fell -0.7%, and the Dow Jones Industrial Average fell -0.94% for the week. |

|

Market News ISM Manufacturing. This week revealed continued contraction in the Manufacturing industry, as the ISM Manufacturing PMI posted at 49% for September, slightly above estimates. September’s PMI reading marked a 2.9% increase from August’s weaker index but remains in contractionary territory overall. All of this comes as certain technical indicators begin to point to a more neutral industrial sector and less of a bearish view on the industry – all of this dependent on macro conditions, which may very well shift to the downside soon. |

|

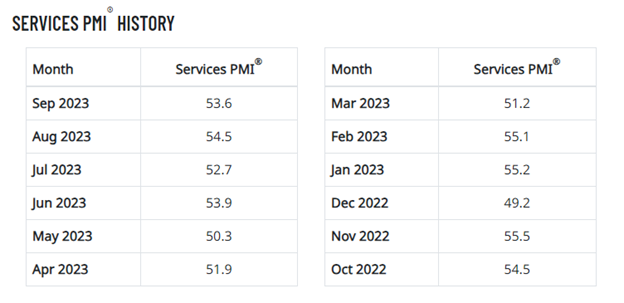

Source: ISM ISM Services. Alongside the ISM Manufacturing Index, the ISM Services Index came out this week, posting another month of growth. The September Services PMI rang in at 53.6%, down slightly from August’s index. Also notable from the report was that the Services Employment Index indicated a hotter employment market, with 85.9% of respondents saying that employment opportunities remained the same or improved in September, something that materialized in September’s strong non-farm payroll data on Friday. |

|

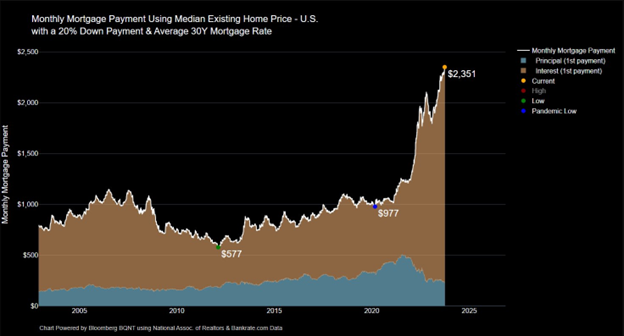

Source: ISM Home Affordability. Buying a home has overwhelmingly become more difficult following the pandemic, as home prices continue to rise and mortgage rates hit 20-year highs. This change becomes strikingly apparent when comparing the payment for the median existing home price in 2020 on an average 30-year fixed mortgage and with a 20% downpayment, amounting to just $977 a month. Compare this with the median existing home price now ($407,100), the average 30-year fixed mortgage rate near 7.5% and a 20% downpayment, the monthly payment skyrockets to $2,351. This rapid shift in affordability for a median home will certainly find its ramifications on the market, however all of its impacts are yet to be seen, particularly with home prices still being quite stable. |

|

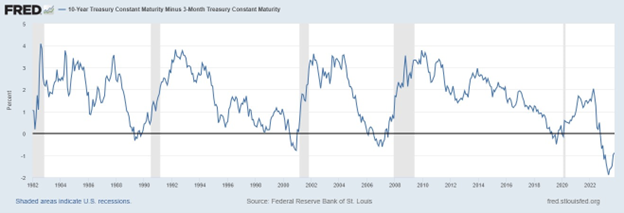

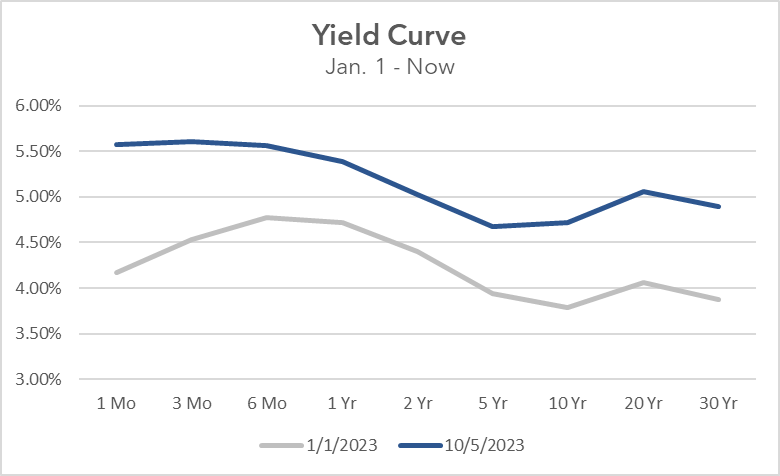

De-Inversion of the Yield Curve. As longer-term US Treasury yields rose this week, the 10-year-3-month yield spread slimmed down, a pre-recessionary indicator. In fact, out of the last four recessions dating back to the 1980s, all four recessions began 3-to-12 months following the de-inversion of the yield curve. In our current situation, the yield curve began de-inverting in June this summer, so a 3-to-12-month lag of a recession should show a recession beginning between now and June of 2024 if history follows its course. |

|

Beyond the recent de-inversion of the yield curve, the yield curve remains much higher than it was at the start of the year, as expectations of higher interest rates have increased throughout the year, particularly following the most recent FOMC meeting where the Fed’s SEP pointed to higher rates in 2024 and 2025. We will continue to keep a keen eye on the yield curve, its de-inversion, and the trend of higher for longer interest rates, along with its implications on markets and our portfolios. |

|

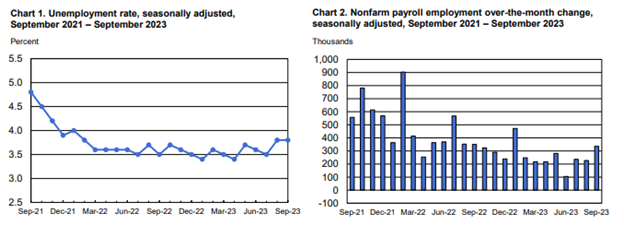

September Employment. Friday’s jobs report for the month of September surprised economists to the upside, clocking in nonfarm payroll +336,000 new jobs in the month, compared to estimates of less than 200,000 jobs. This marked the highest monthly increase of jobs since January this year, making it a notable report for an economy that the Fed wants to slow. On top of nonfarm payroll, the unemployment rate remained the same in September at 3.8% and average hourly earnings rose less than expected at a monthly increase of +0.2%. For an economy many thought would have been in a recession by now, employment markets have not shifted yet, as data continues to show strength in labor conditions. |

|

| Summary This week marked another week of uncertainty, as employment data came in much stronger than expected, the Manufacturing industry appears to be continually sluggish, while the Services industry maintains its strength. Yield curve signals are pointing to a recession by the first half of 2024 as longer-term rates have been rising and de-inverting the yield curve. We look forward to staying agile on this ever-changing macro landscape. We appreciate your continued trust. |

Thank you,  Joseph M. Maas, Joseph M. Maas,CFA, CFP®, ChFC, CLU®, MSFS, CCIM, CVA, ABAR, CM&AA The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Our advisors can meet with you to discuss your retirement plan. |

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.