Market Update – October 13th, 2023

Author: Joe Maas, CIO SPG Advisors LLC

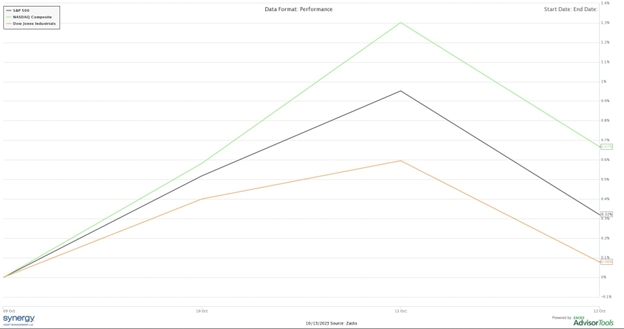

Financial Markets: This week was characterized by inflationary data, the start to Q3 earnings season, along with geopolitical updates in Israel and Palestine. Despite these events, equities ended higher for the week, with the Nasdaq Composite gaining +0.67%, the S&P 500 gaining +0.32%, and the Dow Jones Industrial Average gaining +0.08% as of close Thursday, October 12th. |

|

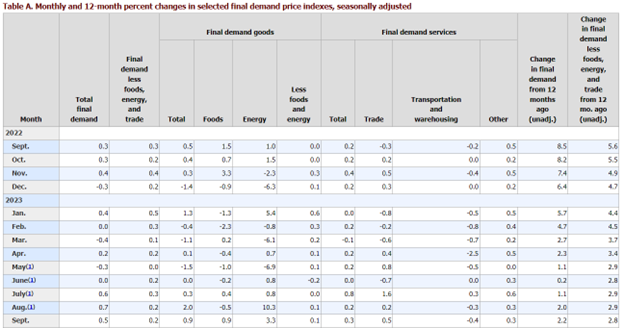

Market News September PPI. September’s Producer Price Index came in hotter than expected, with annual Headline PPI at +2.2% and Core PPI at +2.8%. On a monthly basis, this amounted to an increase of +0.5% in Headline PPI and +0.2% in Core PPI, which marked the lowest month-over-month increase since June, despite the higher annual figures. Driving producer prices higher in September were energy (+3.3% MoM), foods (+0.9% MoM), and trade (+0.5% MoM), while transportation and warehousing (-0.4% MoM) brought producer costs lower for the month. |

|

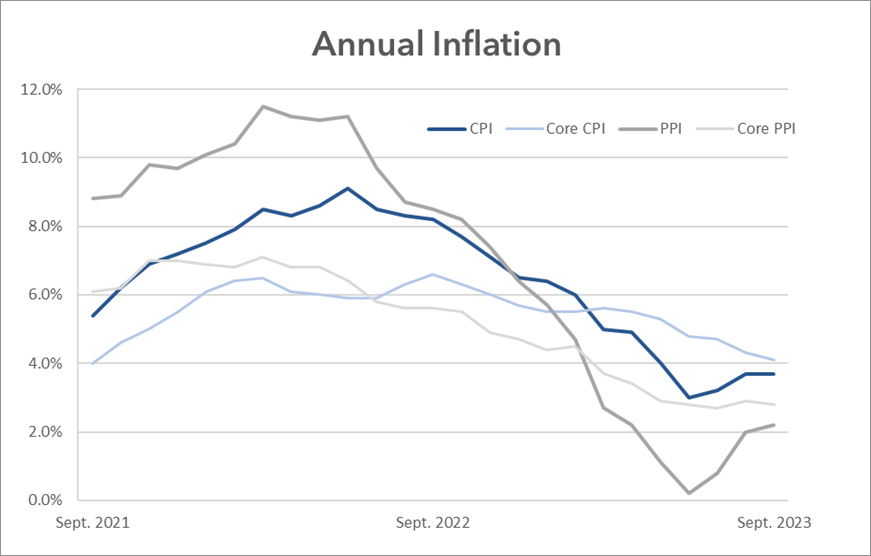

Source: BLS September CPI. Along with the Producer Price Index, the CPI came in slightly higher than expectations at a headline rate of +3.7% annually and a Core CPI rate of 4.1% annually. Month over month, CPI posted at +0.4%, while Core CPI clocked in at +0.3%. This marks another month of moderate inflation, however all measures of inflation for September are still reading in above the Fed’s 2% target, therefore markets must continue to assume higher interest rates for longer, until inflation can get closer to the 2% goal. |

|

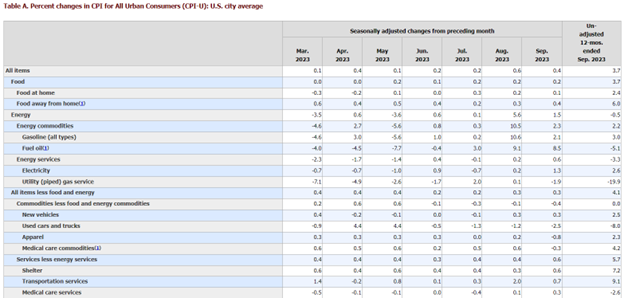

Behind the CPI figures, energy lead the monthly increase in prices for consumers, up +1.1% MoM, alongside transportation services which were up +0.7% MoM and shelter which was up +0.6% MoM. On the other hand, used vehicles (-2.5% MoM) and medical care commodities (-0.3% MoM) were the only two categories down in price in September. |

|

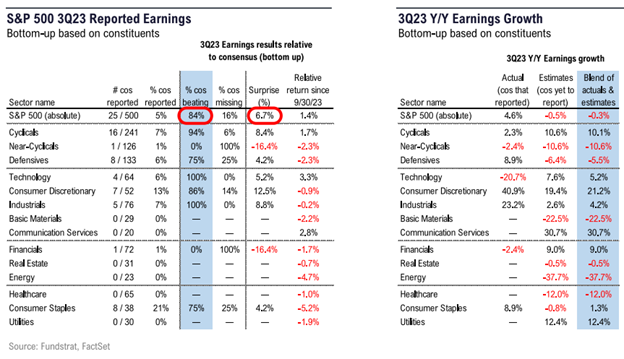

Source: BLS Q3 Earnings Season Starts. This week marked the first of Q3’s earnings season, as analysts expect an annual decline in earnings across the S&P 500. Among the notable reports, JP Morgan Chase & Co, the largest US bank, announced top and bottom-line beats Friday morning. Overall, 5% of the S&P 500 has reported so far, with 84% of those companies’ beating earnings estimates with an average upside surprise of 6.7%. Out of all the sectors, although only 13% of its companies have reported earnings, the Consumer Discretionary sector posts the largest year-over-year earnings growth at +40.9% YoY as of October 13th. We look forward to continuing to monitor Q3 earnings season for insights into various sectors and the larger economic landscape. |

|

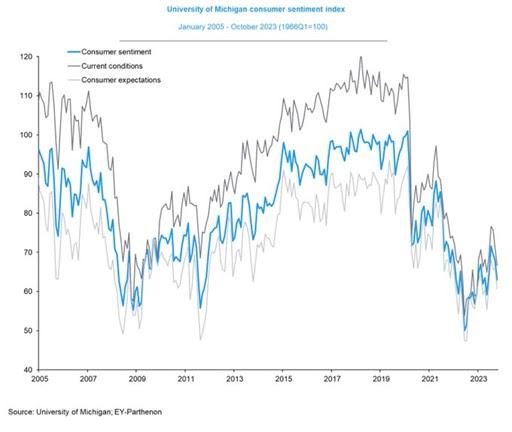

Consumer Sentiment. The University of Michigan’s Consumer Sentiment Index fell more than estimates with a -7.5% month over month drop in October. Alternatively, the university’s Current Conditions Index fell -6.6% and the Consumer Expectations Index fell -8.0% from September’s data. Compared to a year ago, October Sentiment was up +5.2%, Current Conditions were up +1.7%, and Expectations were up +8.0%, however much of this could be attributed to better equity performance this year, as the S&P 500 is up 18% over the last twelve months, as of October 13th. One theme that loomed through respondents’ commentary, was that inflation is still placing pressure on the consumer and negatively impacting household finances, as this week’s CPI revealed annual inflation of 3.7%, almost twice the Fed’s 2% target inflation rate. Although inflation has made significant progress downward, consumers are still feeling the weight of higher prices. |

|

Summary: In a week full of data, inflation continues to clock in above the Federal Reserve’s 2% target, with September’s CPI and PPI indexes both coming in hot this week. Earnings look to be faring well so far for the third quarter, with 5% of the S&P 500 having been reported at this time, largely beating estimates. In other news, consumer sentiment fell in October, as consumers note continually higher prices, like we saw in the CPI. Overall, the economy looks to be in a pivotal position, with higher rates, inflation, and geopolitical risk being in the forefront of investors’ minds. We appreciate your continued trust. |

Thank you,  Joseph M. Maas, Joseph M. Maas,CFA, CFP®, ChFC, CLU®, MSFS, CCIM, CVA, ABAR, CM&AA The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Our advisors can meet with you to discuss your retirement plan. |

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.