How Interest Rate Increases May Affect Your Retirement Savings

February 1, 2022

When the economy is shifting, the big question is always: how does it affect me and what solutions are available to avoid potential negative consequences to my retirement? It’s a question we’re asked frequently, especially by those worried about the effects of rising interest rates.

In 2022, the Federal Reserve raised interest rates four consecutive times in an effort to slow down inflation. Most of us recognize that this creates spending challenges to the everyday consumer. But it also presents challenges to retirees who want long term investments to protect and grow their capital.

Conventional wisdom, or more technically, modern portfolio theory, has dictated for a very long time that in order to preserve capital, one should have an allocation to individual bonds. They are generally considered a “safer” alternative to the volatile stock market. In fact, many bonds have provided solid long-term returns since the general decline of interest rates since the 1980s.

However, it’s important to know what types of bonds you hold.

Individual bonds and bond funds are not the same thing and are affected differently by fluctuating rates.

Individual bonds:

- Are an investment in one entity, usually with a fixed return (the interest rate or “coupon”)

- Maintain their principal, or “par value” as long as the investor holds it to maturity

- The reason many people like holding individual bonds like this is because they know exactly what they are going to get and when.

For example, if John invests $500,000 in a 10-year individual bond with a 5% interest rate, he could generate $25,000 in annual income from the interest he earned, keeping his principal intact. However, at the 10-year mark, interest rates have dropped to 1%. That means that if John reinvested the same $500,000 principal in the same bond, he’d only be able to generate $5,000 in annual income. Coupled with inflation, this is a huge loss of annual income, which could result in significant lifestyle changes for John and his spouse. John would need to be aware of different individual bonds that could provide the same amount of income. However, it takes a significant amount of time to research individual bonds and manage a strategy for the bonds. Working with an advisor can help reduce the burden on you.

Bond funds:

- Bond mutual funds are just like stock mutual funds in that you put your money into a pool with other investors.

- A professional invests that pool of money according to what they think the best opportunities are in accordance with the fund’s stated investment goals. Each type of bond can be affected or controlled differently when the market shifts.

- Bond funds are considered to be more risky and are actually what we see most people are invested in today.

An easy way to understand the impact rising rates have on bond funds is to compare it with refinancing a mortgage. For example, imagine that you took out a mortgage on your home and the only choice you had was a variable, or changing, interest rate. Let’s say your monthly payment was $1,000 and your interest rate started at 3%. Two years later, you get a call from the bank and they tell you that your rate is resetting to the current environment interest rate which is 7%. Your payment is now $2,500. Let’s also say that the real estate market is suffering because people can’t borrow as cheaply so now your $500k house is now worth $300k.

In the same way, when an investor holds 60% of their net worth in a bond fund that they bought at a 1% interest rate, and now the market rate is 5%, the underlying investment (like the housing price) gets significantly reduced in value and they lose money.

One key difference between individual bonds and bond funds is that with bond funds, there’s no guarantee that you’ll recover your principal at a specific time, particularly in a rising-rate environment.

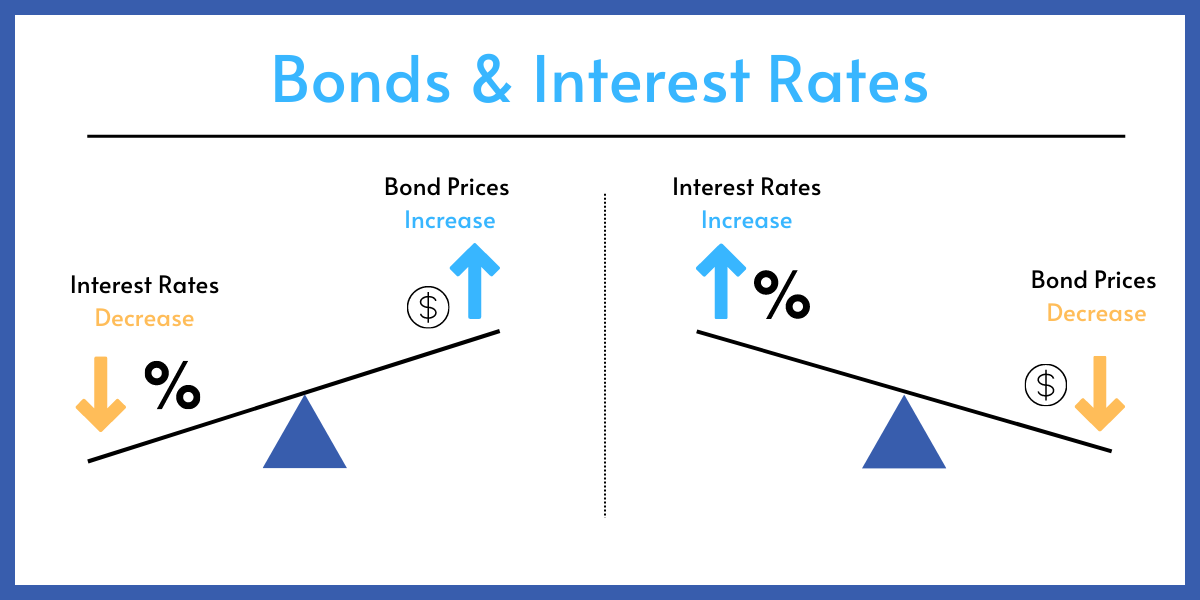

Let’s take a deeper look at the relationship between interest rates and bonds.

Historically, when stocks were losing, bonds were making money, or at least flat, and when bonds were doing poorly, stocks were performing well.

All bonds have a fixed period of time in which they generate income. Their values fluctuate over time due to changing interest rates. When interest rates are increasing, bond values decrease and vice versa. This is known as an inverse relationship.

To fully understand this relationship between interest rates and the value of bonds, it’s important to know what low vs. high interest rates represent. In a healthy and properly functioning marketplace, interest rates act as economic thermometers.

Lower interest rates dictate less risks for businesses or households. Businesses are willing to expand since they can get loans at lower interest rates and it’s likely that consumers have more buying power. This often leads to a booming economy, like what we saw in the US during Covid-19.

Higher interest rates dictate elevated risks for businesses or households. Companies in poor economic condition have to sell their bonds at very attractive rates because there is a risk of them defaulting on their loans. Classically, when interest rates are elevated, it signals to the marketplace there are less savings, people incurring more debt, and businesses are reluctant to expand because consumers are not in a great position. In other words, it creates a recessionary environment, and this is exactly what we are seeing right now.

Currently, the biggest impact for retirees is the consequences of the leap from a 1% interest rate to a 6% rate over the past year. Why? Retirees have usually been taught to fill their portfolios full of bonds, and when rates rise, their bond principal suffers.

So who’s better off?

The investor who puts $500k in an individual bond at 5% interest and is able to generate $25k in income each year?

OR

The investor, who, in 2019, invested in a target date retirement mutual fund that lost 18% by 2022?

If the purpose of bonds was preservation of principal, then bond funds simply are no longer the best option, especially to those nearing or in retirement. The downside one can experience in exchange for very little upside is not a profitable trade-off.

While individual bonds can be a good source of fixed income, they don’t come with any guarantees like you may have been taught. If you are nearing or in retirement, you may be evaluating your options for ways you can protect your money in a time where the market is volatile.

All of the pros and cons for individual bonds and bond funds need to be placed into the context of your preferences and circumstances. What works well for you might not work well for others, and vice versa. There are several important considerations when determining whether an individual bond or bond fund is best for you: the amount you have to invest, your financial goals, and your behavioral preferences.

After experiencing big losses in their bond funds this past year, some investors are wondering if they would have been better off holding individual fixed-income securities.

Alternatives for bonds funds include, but are not limited to:

- Treasury bills and bonds

- High-yield Certain certificates of deposits

- Highly-rated individual bonds

- Fixed annuities

It’s best to consult your financial advisor to determine the best course for you and your goals.

We are here to help people put all the pieces of their financial puzzle together and make sure your financial plan evolves as your life unfolds. We will help you clarify your objectives, quantify your goals, and identify situations you would like to avoid. With this mindset and knowledge, we can help you determine the investment tools to use that will best meet your needs.

Want to know more about your options to achieve your long-term financial goals?

Make an appointment with Sound Planning Group, an independent advisory firm, by calling us at 425-821-9442 or visiting: https://myspg.com/schedule/

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.