A Brief Commentary on Q1 2023

Author: Joe Maas, CIO, SPG Advisors, LLC

QUARTERLY COMMENTARY

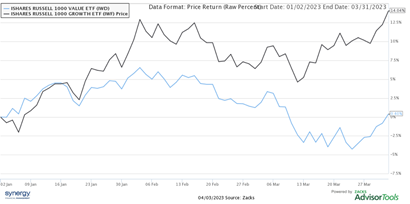

Q1 of 2023 brought positive returns in both the S&P 500 (+7.03%) and the Nasdaq Composite (+16.77%), with a muted Dow Jones Industrial Average (+0.38%). Accordingly, Q1 saw a major shift towards growth stocks, unlike in Q4 of 2022, as the Russell 1000 Growth gained strong +14.04%, while the Russell 1000 Value gained a meek +0.40%, which is also apparent in the Dow’s performance compared to the Nasdaq’s. Two of out of three of the largest bank failures occurred on the weekend of March 10th to March 12th, with the collapses of Silicon Valley Bank and Signature Bank. The FDIC, Federal Reserve, and US Treasury backed all deposits at these two banks and offered all FDIC insured banks short term liquidity assistance through the Bank Term Funding Program. Internationally, Swiss Bank Credit Suisse faced similar difficulties and saw a speedy acquisition from UBS, as Swiss regulators rushed to get a deal done before a full bank failure.

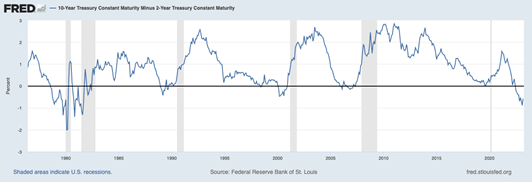

As depositors fled to safety in US Treasuries through mid-March, yields on the closer end of the curve fell rapidly. Specifically, we saw the 2-year US Treasury market yield fall from over 5% in early March to under 4% in late March. The 10-year minus 2-year US Treasury spread continued to demonstrate concern of a recession in Q1, as economic downturns historically have followed negative spreads, especially when they remain over -0.50% like the current spread. Note this 10-to-2-year UST spread chart, where a spread this extreme hasn’t happened since the early 1980s, over 40 years ago. Q1 yields remained strong on cash and equivalents though, as investors find comfort in guaranteed 4% returns.

Economic data in the first quarter of 2023 showed signs of a slight slowdown, but ultimately came in hotter than expected in most circumstances. CPI inflation for December of 2022 to February of 2023 came out during the quarter falling from December’s +6.4% YoY inflation to February’s +6.0% YoY inflation. The more encouraging data point of inflation came from PPI, which is often thought of as a leading indicator of inflation, as producers tend to pass down higher costs to consumers. Q1 brought us PPI data for December through February as well, falling from December’s high +6.5% PPI inflation to February’s much lower +4.6% PPI inflation. Employment data remained strong in Q1, with an unemployment rate of 3.6% in February, up slightly from January’s historically low unemployment rate of 3.4%. Corporate earnings in Q1 revealed varied performance from 2022, depending largely on industry and company.

The Synergy team implements a variety of fundamental, technical, and macroeconomic analysis when evaluating and shifting our portfolios. We paid additional attention to the macroeconomic environment, as well as specific company performance, such as exposure to financials or real estate, particularly in relation to interest rate risk. In Q1, one key shift in markets was back to growth focused equities, while in Q4 of 2022, the opposite was true. In both cases, our analysts are constantly evaluating opportunities within the marketplace. Certain changes are permanent in nature, while some are more opportunistic for the current macroeconomic environment. Our portfolios will continue to be actively monitored and adjusted as necessary per each portfolio’s mandate.

Looking Forward

As always, we are closely tracking inflation, the Federal Reserve, interest rates, corporate earnings, and geopolitical events. Inflation, particularly PCE inflation, will be a key determinant moving forward, as this remains the Federal Reserve’s target metric in their monetary policy decisions. We will be closely monitoring the next two Fed meetings, as markets are currently expecting a Federal Funds rate hiking pause on either the May 3rd or June 14th FOMC meetings. As of March 31st, 2023, markets are pricing in a 51.4% probability of a rate pause on May 3rd and a 48.6% probability of another 25-bps rate hike. US Treasury rates will continue to be a notable metric, along with mortgage rates, as each of these holds far reaching implications in financial markets.

We look forward to getting more insight on company earnings as Q1 earnings will kick off with the largest banks in April. Other industries such as consumer discretionary, real estate, and technology will reveal more about how consumers are feeling in this current macroeconomic environment. On top of these factors, we are paying additional attention to the domestic and international banking environments, along with any lending contraction in credit markets that may hold implications on wider economic growth. Other geopolitical events will be equally as important, particularly in regard to energy and commodities.

SPG looks forward to continuing to monitor this unique time in the financial markets.

Your team at Sound Planning Group

The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Our advisors can meet with you to discuss your retirement plan.

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.