Deciphering the Tax Implications of Social Security and Retirement Accounts

April 1st, 2024 by Sound Planning Group

Navigating the maze of taxation on retirement income is a task that many retirees find daunting. The complexities of how Social Security benefits, pensions, and withdrawals from retirement accounts are taxed can significantly impact one’s financial stability in retirement. Understanding these complexities is crucial for devising forward-thinking strategies that anticipate tax obligations. This allows you to adjust withdrawal plans accordingly before it’s too late, ensuring a more secure financial foundation during one’s golden years.

Understanding Social Security Benefits Taxation

Navigating the maze of taxation on retirement income is a task that many retirees find daunting. The complexities of how Social Security benefits, pensions, and withdrawals from retirement accounts are taxed can significantly impact one’s financial stability in retirement. Understanding these complexities is crucial for devising forward-thinking strategies that anticipate tax obligations. This allows you to adjust withdrawal plans accordingly before it’s too late, ensuring a more secure financial foundation during one’s golden years.

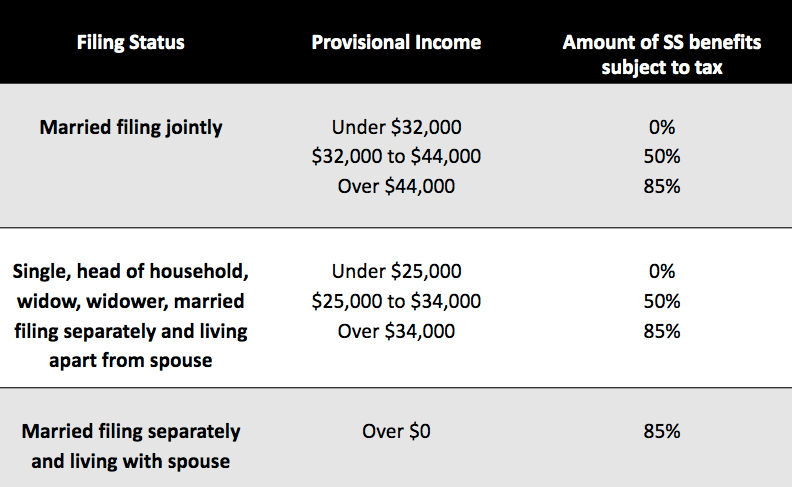

Social Security is taxed based on your other income sources through an equation called “Provisional Income.” You first calculate what 1/2 of your Social Security benefits are, then you add all other taxable income, including dividends and realized capital gains, interest, plus non-taxable interest earnings, such as from municipal bonds.

Chart A: Provisional Income Calculation

Once we have calculated Provisional Income, it’s time to apply the thresholds. The key here is that only the Provisional Income that falls over the threshold creates taxable Social Security.

Chart B: Social Security & Provisional Income

Taxation of Pensions and Retirement Account Withdrawals

Pensions and withdrawals from retirement accounts add another layer of complexity to retirement taxation. Traditional IRAs and 401(k)s offer tax-deferred growth, meaning taxes are paid only upon withdrawal.

In contrast, Roth IRAs and Roth 401(k)s are funded with after-tax dollars, allowing for tax-free withdrawals in retirement. The strategic timing of these withdrawals can significantly influence your tax liability and the longevity of your retirement savings.

Balancing withdrawals from tax-deferred and tax-free accounts can help manage your taxable income and potentially reduce the taxes owed on Social Security benefits.

Strategies for Anticipating Tax Obligations

Strategy #1:

One strategy that you may consider given the favorable tax environment that we find ourselves in today, is to delay claiming Social Security until later while using your tax-deferred retirement accounts first.

This would allow your Social Security to gain a guaranteed 8% per year in delayed credits plus any Cost of Living Adjustments (COLA).

Then, coupled with your Social Security benefits and various withdrawals at age 70, you could potentially gain a more tax-efficient income for the rest of your life!

In general, many people would benefit from waiting until age 70 to take Social Security. Others may need the income sooner and may lack the resources necessary to meet expenses during the delay period, or they may not live long enough to reap the rewards of delaying their claim.

There is no question that it is critical to get competent help, given the difficulty of reversing Social Security elections and the value that can be created by coordinating your various income sources.

Strategy #2:

Another strategy to reduce the taxes you pay on your Social Security income involves converting traditional 401(k) or IRA savings into a Roth IRA.

A method to potentially trim down the taxes on your Social Security proceeds is by transforming standard 401(k) or IRA savings into a Roth IRA.

The versatility to contribute to a Roth IRA or Roth 401(k) might be unavailable due to specific income limits set by the IRS, yet there’s a chance of tapping into the tax-free growth and tax-free withdrawal benefits of a Roth IRA. This can be done by transferring currently existing funds from a traditional IRA or an employment-based retirement savings account into a Roth IRA, a tactic referred to as a partial Roth conversion.

The amount you’re allowed to convert from your conventional IRAs is flexible, providing you an opportunity to control the tax implications of this conversion. Besides the attractive feature of possibly tax-free withdrawals, these accounts won’t affect the tax status of your Social Security benefits, a key attribute many individuals tend to overlook.

It’s crucial to keep in mind that the sum you opt to convert is typically deemed taxable income. Therefore it might be wise to convert only the amount that could place you at the peak of your current federal income tax bracket. Additionally, you might want to decide the conversion amount based on the probable tax obligations to enable you to cover your tax bill using cash from a non-retirement account. To ensure you make the most appropriate decisions, it’s recommended to seek advice from a tax professional.

Factors to Consider When Claiming Your Social Security:

There’s a lot of factors to consider when deciding to claim your benefits. Here are some you should be aware of:

- Life span – The potential “breakeven points” of delaying or taking benefits.

- Spousal Benefits – Age differences and the effect on future widow benefits

- Retirement goals – Savings, retirement age, desired budget, pension options, coordinating the “Income-Gap” between FRA and 70, etc.

- Tax – The preferential treatment of your SS income.

- Retirement assets – If you have large 401k/IRAs with small Roth or After-Tax accounts, this strategy might make a significant difference for you.

Here’s What You Can Do:

- Understand the Income Thresholds: Familiarize yourself with the income thresholds that trigger taxation on Social Security benefits.

- Plan Withdrawals Wisely: Consider the timing and source of your withdrawals. Withdrawing from a Roth account during years of higher income can minimize your overall tax burden.

- Stay Informed on Legislative Changes: As noted by the Social Security Administration, the maximum amount of earnings subject to Social Security tax can change annually. Keeping abreast of these changes is essential for effective tax planning.

Tax laws and regulations are continually evolving. Consulting with a tax professional or financial advisor who can provide personalized advice based on the latest rules and your unique financial situation is always a wise decision.

By understanding the tax implications of Social Security benefits, pensions, and retirement account withdrawals, retirees can better navigate the complexities of retirement taxation. Implementing strategic tax planning techniques can lead to significant savings, maximizing the net amount received from these sources and ensuring a more financially secure retirement.

If you would like to learn more about these topics, join us at an educational course taught near you:

Course: Taxation of Social Security

The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Consult with your investment advisor, legal, non-financial planning tax specialist, or estate professional prior to making any financial decisions for your personal situation. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment or investment strategy (including those undertaken or recommended by SPGA), will be profitable or equal to any historical performance level(s). Our advisors can meet with you to discuss your retirement plan. We’re here to help with all of these things and more.

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.