Market Update – April 15th, 2024

Author: Joe Maas, CIO SPG Advisors LLC

Monday, April 15th, 2024

Financial Markets

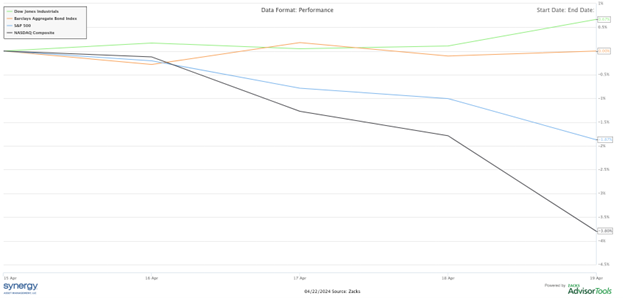

Markets continued a pullback last week on news of rising geopolitical tensions and strong US retail sales data. As of Friday, April 19th, the Nasdaq Composite fell -3.8% and the S&P 500 fell -1.87% in the week, while the Barclays Aggregate Bond Index ended flat. On the other hand, the value-heavy, price weighted Dow Jones Industrial Average rose +0.67%, with its most heavily weighted stock, United Health Group up +12.45% last week on a strong earnings report.

Market News

Retail Sales:

March’s retail sales showcased robust consumer spending, defying expectations and demonstrating the economy’s resilience amid a restrictive monetary policy backdrop. Despite mounting inflation, consumer spending exceeded projections, with retail sales marking a significant monthly increase of +0.7%. Excluding auto sales, the surge was even more pronounced, with retail sales climbing by +1.1% in March. On an annual basis, retail sales were up +4%, outpacing the annual CPI inflation rate of 3.5% for March.

The uptick in retail sales was broad-based, with higher energy prices notably contributing to the increase, as gas stations reported a notable monthly surge of +2.1% in. Additionally, online sales led the rise in retail sales, surging by +2.7% from February and an impressive +11.3% from March 2023. On the other hand, sectors like auto sales, sporting goods, and electronics experienced monthly declines. Overall, the strength reflected in this month’s retail sales report suggests that the health of the US economy may delay the widely anticipated Federal Reserve rate cuts.

New Residential Housing:

The shortage of residential housing remains a significant driver of inflationary pressures, as highlighted by the March Consumer Price Index showing a 5.7% annual increase in shelter costs. However, March saw housing permits and starts fall short of expectations, with new permits -3.4% lower than expected and housing starts -10.7% lower than expected. Despite missing estimates, new building permits still reached 1.458 million, while housing starts totaled 1.321 million and completions stood at 1.469 million. These numbers more closely resemble pre-pandemic residential construction volumes.

There is optimism that potential interest rate cuts by the Federal Reserve in the coming year could alleviate pressure on builders, as interest rates become less burdensome. This, in turn, may stimulate a more rapid increase in residential supply, which would also contribute to addressing inflationary pressures in shelter costs.

Existing Home Sales:

Existing home sales data for March met expectations, with 4.19 million homes sold during the month, marking a decline of -4.3% from February and -3.7% from the previous year. Inventory levels showed an increase compared to the previous year, reaching 3.2 months of supply.

Prices saw a modest rise as anticipated, with the median home price increasing by +4.8% compared to the previous year, surpassing overall inflation rates. Ultimately, much of the stagnant nature of existing home sales stems back to the lack of significant movements in interest rates.

Source: National Association of Realtors

Leading Indicators:

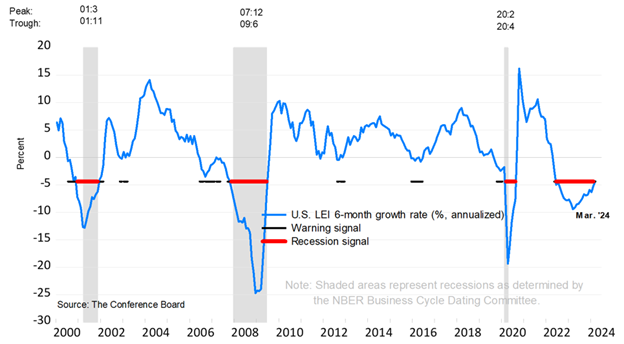

The Leading Economic Index (LEI) is an early indicator of significant potential turning points in the business cycle and where the economy may be heading in the near term. However, March’s LEI data fell slightly below expectations, recording a decline of -0.3%. This downturn was primarily influenced by bearish trends in the yield curve, along with weaknesses observed in building permits, consumer sentiment, and new orders. These leading indicators collectively paint a cautious picture for the US economy, signaling a recession to come if historic norms follow through. Despite this bearishness in the LEI, the broader economic conditions have yet to demonstrate a substantial deterioration.

Empire State Manufacturing Survey:

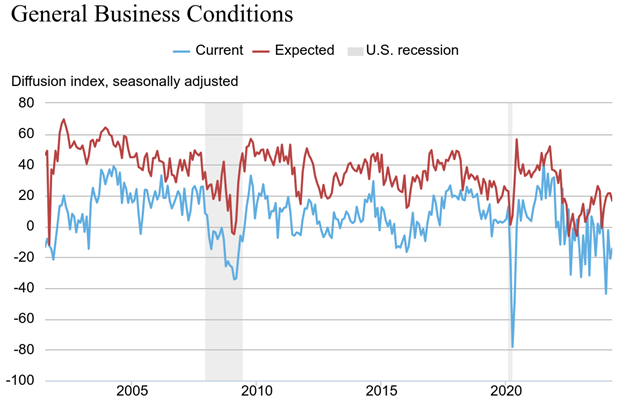

The Empire State Manufacturing Survey, conducted monthly by the Federal Reserve Bank of New York and providing a read on one of the most economically significant states in the US, New York, offers a valuable snapshot of the manufacturing sector’s health. For the month of April, economists expected that the General Business Conditions Index within this survey would rebound to -10, however, the index only rose to -14.3. Despite a slight uptick from March, this reading fell short of expectations and continues the trend of an index below zero, indicating ongoing challenges within the sector.

One economic researcher at the New York Federal Reserve summarized the state of manufacturing like this: “Manufacturing activity continued to contract in New York State in April, and employment continued to decline. Optimism about the outlook for future business conditions remained subdued.”

Multiple indicators, including the General Business Conditions Index from the NY Federal Reserve, point to persistent sluggishness within the manufacturing sector. In fact, some of these metrics, including the Empire State Survey, suggest that the sector is currently operating in conditions close to those observed at the onset of the 2007 financial crisis, as seen below. Despite this, broader readings of economic health, like GDP and employment suggest a much more positive picture.

Source: NY Federal Reserve

Summary

Geopolitical tensions and strong US retail sales data prompted a pullback in stocks lasts week, as the Nasdaq Composite and S&P 500 declined, and the Dow Jones Industrial Average rose slightly on UNH’s strong quarterly earnings report. March’s retail sales exceeded expectation, sending expectations of the Fed’s first rate cut further into the second half of the year. The new residential housing market faces challenges with permits and starts falling short in March, as existing home sales volumes also dipped, reflecting stagnant market conditions amidst minimal interest rate movements. The Leading Economic Index recorded a slight decline, signaling cautious economic conditions, while the Empire State survey also signals cautiousness in the manufacturing sector.

Thank you,

Joseph M. Maas,

CFA, CFP®, ChFC, CLU®, MSFS, CCIM, CVA, ABAR, CM&AA

The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Our advisors can meet with you to discuss your retirement plan.

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.