Market Update – August 11, 2023

Author: Joe Maas, CIO, SPG Advisors, LLC

Published August 11, 2023

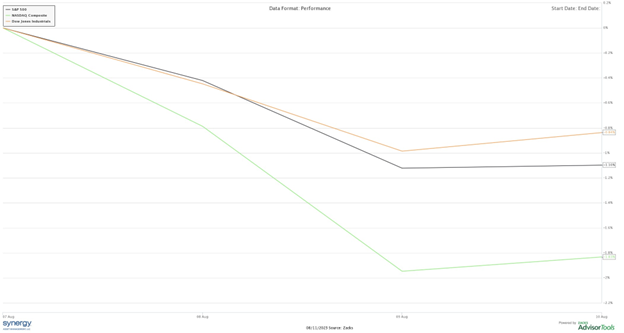

Financial Markets: Even though we are bit far from the next FOMC meeting in this Fed-centric economy, all eyes were on inflation prints, as well as the unexpected credit downgrades of 10 small & mid-sized banks this week as equities saw large intraday swings. As of close Thursday, August 10th, the Nasdaq Composite was down -1.83%, the S&P 500 was down -1.1%, and the Dow Jones Industrial Average was down -0.84% for the week. |

|

Market NewsBank Downgrades. Following Fitch’s downgrade of the United States’ credit rating, this week another prominent credit rating agency, Moody’s, downgraded 10 small and regional sized banks’ credit ratings. Additionally, Moody’s cited that they were reviewing 6 other banks and changed the outlook on 11 banks from stable to negative. Moody’s reasoning for the actions largely revolved around higher funding costs, limited loan growth, possible commercial real estate underperformance, and continued interest rate risk. At this point, the team is viewing the impacts of these recent downgrades as simply short-term catalysts in markets, however, will continue to closely monitor the situation. |

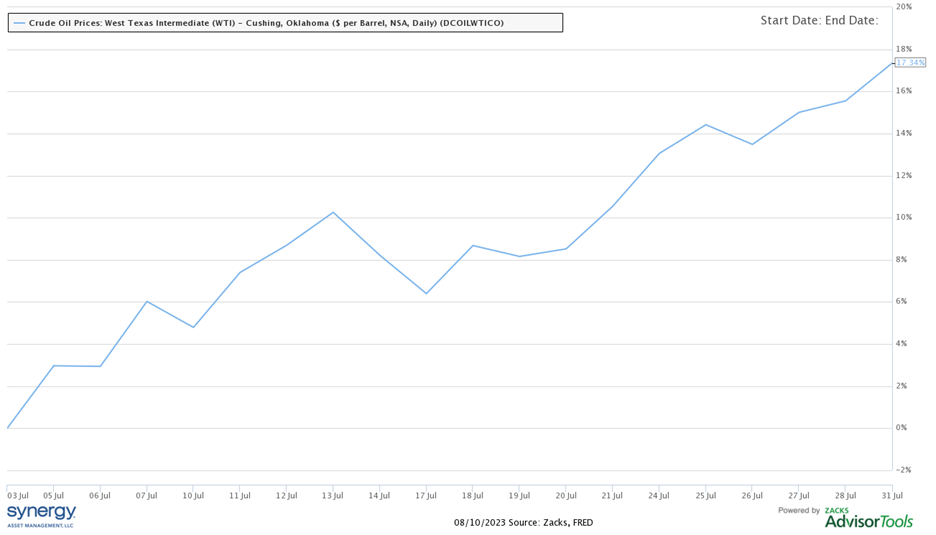

Oil Prices. You may have noticed a higher price at the pump over the last few weeks and wondered what is driving these increased prices. The reason behind the recent oil price rally sits in a commonly known economic phenomenon that we often overlook – supply and demand. With global supply cuts from Saudi Arabia and Russia, paired with increased travel and robust demand, the recent rally in oil prices has become a simple equation of squeezed supply and heightened demand, with prices up over +17% in the month of July. Looking ahead, we cannot tell completely how oil commodity markets will move, however encouraging signs for consumers, such as the lower production cut Russia has announced for September seem optimistic that prices will not continue to spike. |

|

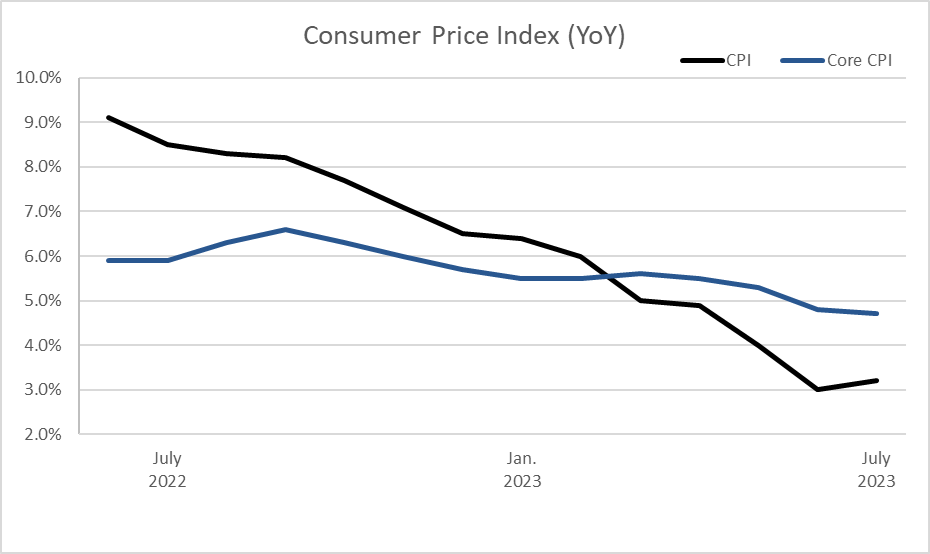

July’s CPI. The Consumer Price Index for the month of July posted on Thursday morning this week, with Headline CPI at +3.2% and Core CPI at +4.7% from a year ago. On a monthly basis, both Headline and Core CPI amounted to +0.2%, surprising economists to the downside. Markets were encouraged by the data, with the S&P 500 popping more than a percent Thursday morning on the news. |

|

What drove the July inflation report was largely shelter costs, which were up +7.7% compared to July of 2022, despite higher interest rates. Other inflationary catalysts included transportation services, which were up +9.0% from last year, as well as food away from home, which was up +7.1% from a year ago. Pulling July’s Consumer Price Index lower was energy products (-12.5% YoY), used vehicles (-5.6% YoY), and medical care services (-1.5%). We are encouraged by this CPI report and look forward to inflationary pressures approaching the Fed’s 2% target inflation rate. |

|

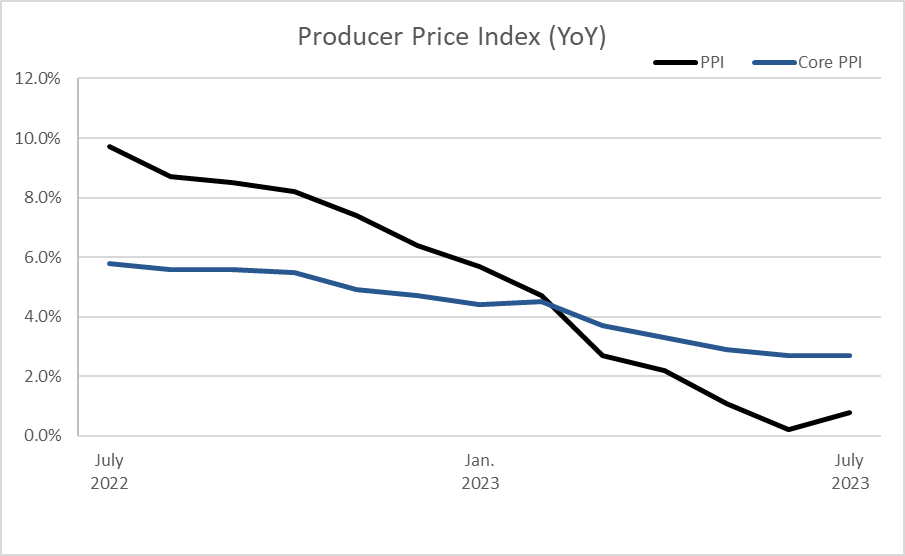

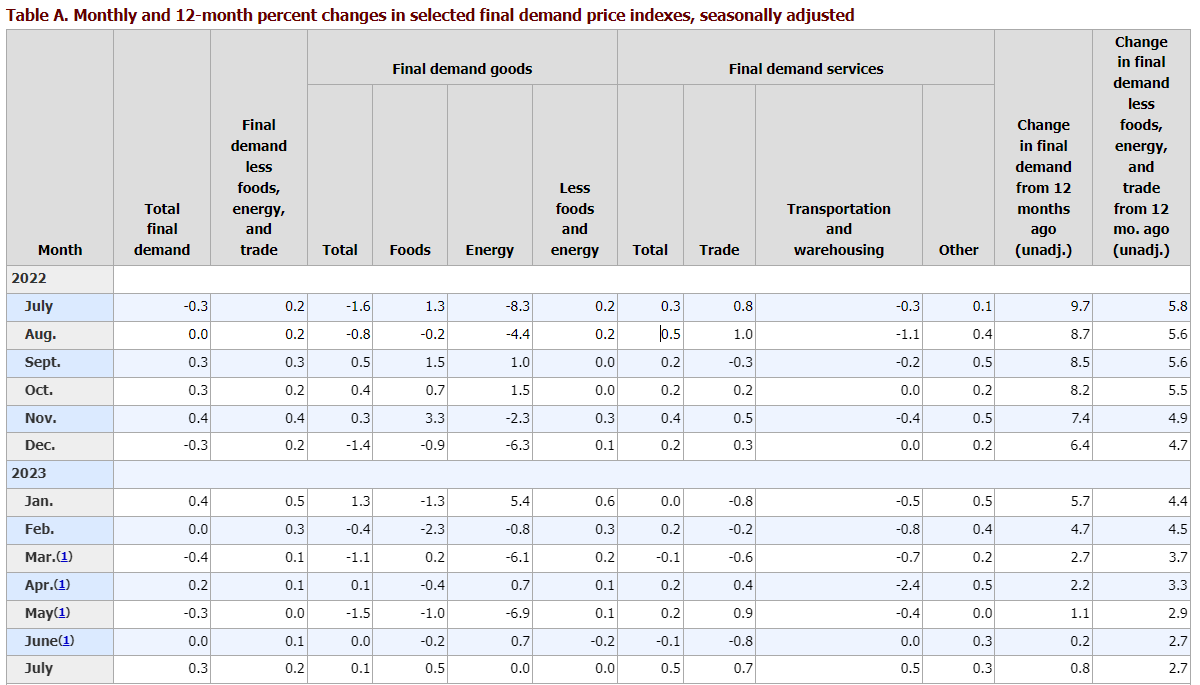

Source: BLS July’s PPI. Along with the CPI for July, the Producer Price Index was also released, coming in ever so slightly hotter than expected. Headline PPI was up +0.8% and Core PPI was up +2.7% in July, compared to a year ago. On a monthly basis, Headline PPI rose +0.3% in July, as Core PPI picked up +0.2%. |

|

Behind this small uptick from June, were higher food (+0.5% MoM), trade (+0.7% MoM), and transportation and warehousing costs (+0.5% MoM), balanced out by lighter inflation in the overall final goods category (+0.1% MoM) and flat energy costs to producers from last month. Between CPI and PPI, inflation appears to be trending in the overall right direction, however we will continue to monitor these data points closely as they roll out. |

|

Source: BLS Consumer Sentiment. The University of Michigan’s Consumer Sentiment Index demonstrated consumers’ continued bullishness, as the index remained relatively unchanged in August, but is demonstrating a strong upward move since late 2022. Additionally, August’s Index amounts to a +22.3% increase in sentiment versus one year ago, a good sign as of now for economic conditions. |

|

Summary Inflation continued to show disinflationary signs this week with July’s CPI and PPI figures coming in, as small & mid-sized banks were downgraded by Moody’s and surprised investors. Additionally, we saw that consumers are feeling more encouraged by economic conditions as seen in the University of Michigan’s Consumer Sentiment Index, despite oil prices rising in July. In every economic environment, we look forward to continuing to monitor markets closely. We appreciate your continued trust. |

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.