Market Update – December 22nd, 2023

Author: Joe Maas, CIO SPG Advisors LLC

Friday, December 22nd

Friday, December 22, 2023

Financial Markets

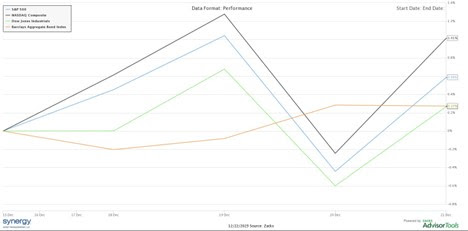

This holiday week came with vital economic data that continues to paint a mixed picture of the economy, as stocks continued their rally. As of close on Thursday December 21st, the Nasdaq Composite was up +1.01%, the S&P 500 was up +0.58%, the Dow Jones was up +0.27%, and the Barclays Aggregate Bond Index was up +0.27% for the week.

Market News

Existing Home Sales. November existing home sale volumes exhibited the first monthly increase in the last six months but are still down significantly from the pre-rate hike norms. Existing homes sold in November totaled 3.82 million, up +0.8% from a month ago, but -7.3% below November 2022’s levels. Average inventory is up to 3.5 months compared to 3.3 months a year ago, suggesting that homes for sale are sitting on the market for longer. Also in this report, the median sales price of an existing home across the US came to $387,600 in November, a modest inflationary rate of +4.0%.

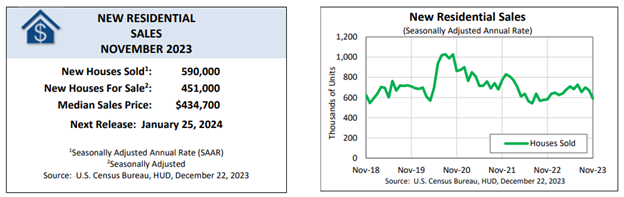

New Home Sales.

Alongside existing home sales data, new homes sales data for the month of November was released this week, showing a +1.4% increase in volume compared to a year ago, totaling 590,000 new homes sold. The median sales price of a new home was down -5.97% from a year ago, but still at a lofty $434,700, while the average new home price sat at $488,900. All of this comes at a very dynamic time where mortgage rates have fallen sharply over the last two months, with the average 30-year mortgage rate peaking at 7.79% on October 26th and slipping to 6.67% on December 21st, marking a -14.4% decline in a short period of time.

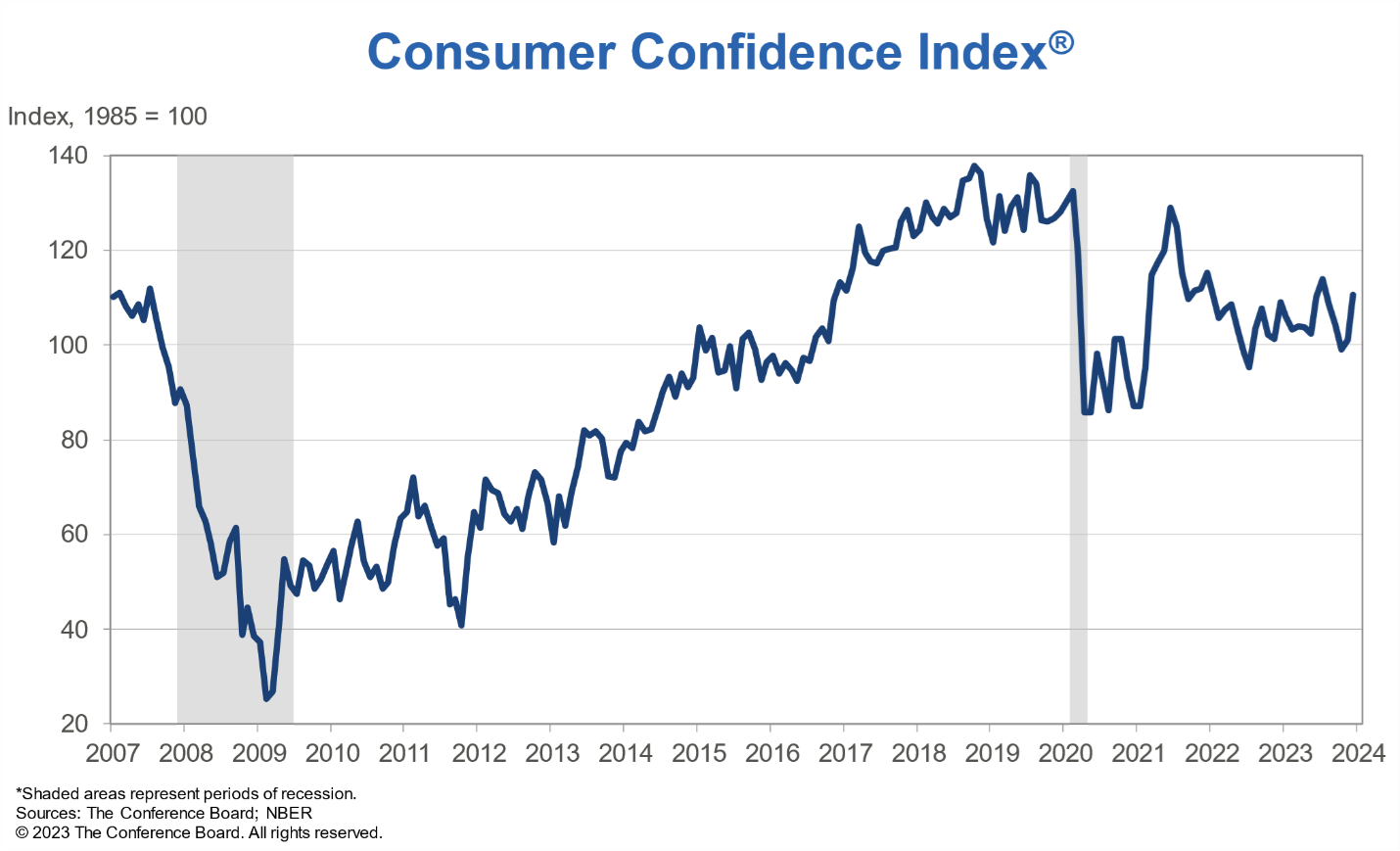

December Consumer Confidence.

With the Santa Clause rally and holiday spirit, consumers are feeling more confident in the economy in December. The consumer confidence index rose +9.6% in December compared to a month ago, with the largest gains in confidence among those aged 35-54 and earning at least $125,000 per year. The expectations index jumped +10.6% from November, insinuating that consumers are feeling more optimistic about the new year. Consumer confidence remains below pre-pandemic levels, however, is not near recessionary levels in any regard either. We look forward to continuing to analyze consumer views in this interesting macroeconomic environment.

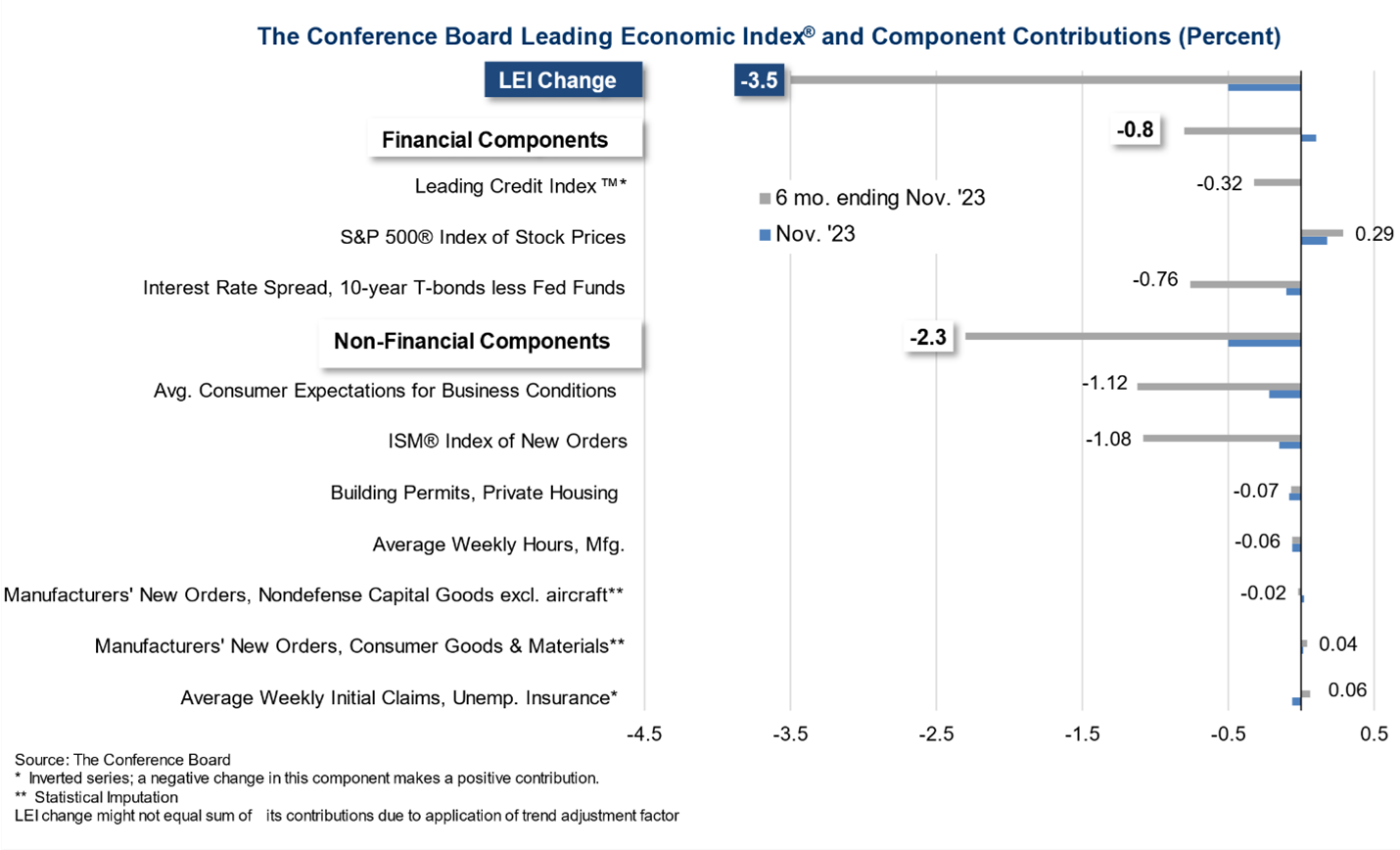

Leading Indicators.

November’s Leading Economic Index declined -0.5% in the month, following a -1.0% decline in October. Influencing this month’s bearish outlook, were lower consumer expectations for business conditions, a sluggish ISM index of new orders, and a continually inverted yield curve. Positively influencing leading indicators was primarily the rising S&P 500, which was up +8.9% in November. Leading indicators have painted a bleak picture of economic conditions to come, however little data has so far suggested that we are in a recession by any means.

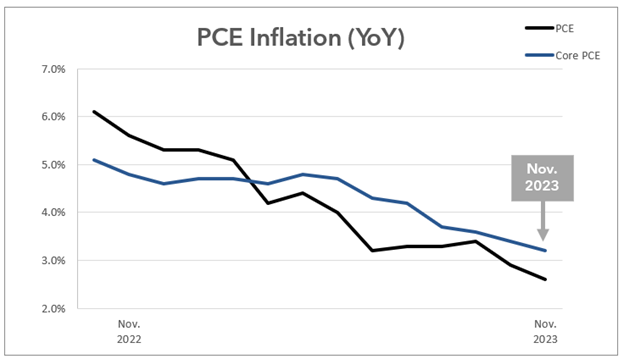

November PCE Report.

In the November Personal Consumption Expenditures report, headline PCE inflation experienced a monthly decline of -0.1%, marking the first monthly decrease in prices since 2020. Meanwhile, Core PCE exhibited a modest increase of +0.1% on a month-over-month basis in November. On an annual basis, PCE inflation ran at just 2.6%, reflecting a very moderate rate, while Core PCE saw a slightly higher figure at 3.2%. Both headline and Core PCE demonstrated significant strides in November towards the Fed’s 2% target inflation.

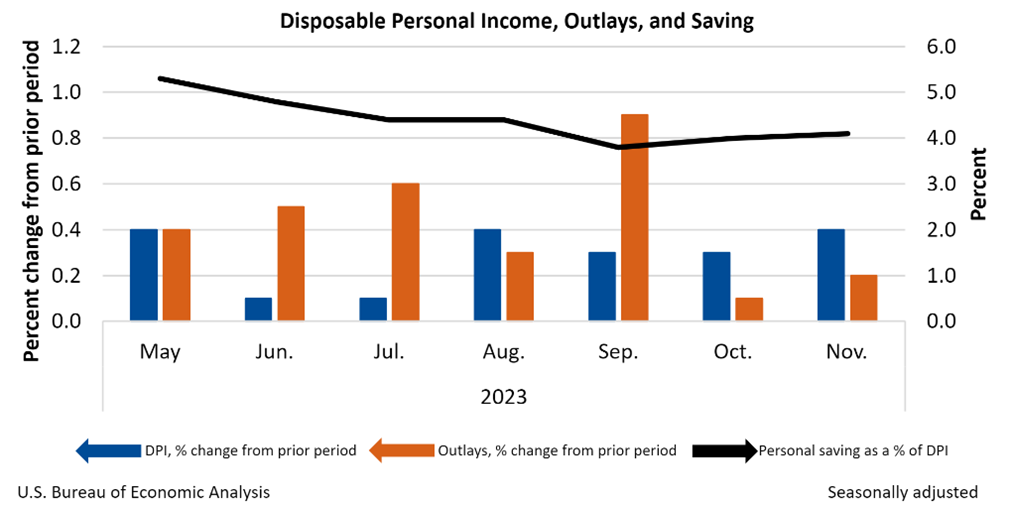

Also in the PCE report, November personal income grew by a monthly rate of +0.4%, surpassing inflation, while disposable income increased by +2.0%. Personal outlays rose by +1.0%, indicating heightened spending, while the personal savings rate saw a slight uptick to 4.1%, signaling a balance between consumption and saving. We are encouraged by this latest PCE report, particularly with inflation slowing down significantly.

Summary

Amidst a holiday week, economic indicators presented a mixed outlook as stocks continued their rally. Existing and new home sales continue to show the impacts of higher mortgage rates, with sluggishness in both markets. December’s consumer confidence rose significantly in the month, however on the other hand, leading economic indicators for November declined, demonstrating a disconnect between current and forward looking indicators. In the November PCE report, headline inflation dropped -0.1% from October to November, the first month of deflation we’ve seen since 2020. Annual PCE inflation rates also cooled more than expected.

We appreciate your continued trust.

The information contained herein is general in nature. It does not take into account your particular investment objectives, financial situation, or needs. It is provided for illustrative or informational purposes only, and should not be construed as advice. Our advisors can meet with you to discuss your retirement plan.

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.